-

Redaction

Redaction

Why the 2% inflation target favors gold long term

Thomas Keller breaks down the mechanics of the 2% inflation target, the 1971 gold-dollar split, and why gold remains the classic debasement hedge today.

This article presents Thomas Keller's analysis, interpretation and personal perspective on monetary policy, inflation and asset preservation. The views expressed do not necessarily represent a universal consensus among economists or financial institutions. Economic systems are complex and different experts may interpret the role of inflation, central banks and hard assets in different ways. This article is intended for informational and educational purposes only and should not be considered financial advice or a recommendation to buy or sell any asset.

To understand the modern financial landscape, you have to recognize that the stability we're promised is a controlled burn. Central banks globally, from the Federal Reserve to the European Central Bank, have institutionalized a policy of gradual currency destruction under the banner of the 2% inflation target. Economists present this as a stability tool. For the investor and the saver, it functions as a mandatory annual fee on liquidity. That structural reality creates a widening chasm between sovereign paper and hard assets, gold specifically. Here's how the mechanics of that divergence work, and why 2% is really just the floor for long-term currency debasement.

The architecture of the 2% mandate

Central banking logic holds that zero percent inflation is dangerous. The fear is a deflationary spiral: falling prices lead consumers to delay purchases, corporate revenues collapse, layoffs follow, and demand shrinks further in a self-reinforcing loop. The 2% target exists as a buffer against that outcome. But this number isn't a law of physics. New Zealand's finance minister floated it almost offhandedly during a 1988 television interview, and the country's central bank later formalized it as policy. It wasn't the product of exhaustive empirical modeling. It became a global standard because it worked well enough, and because it gave central banks room to maneuver.

That room is the real point. In a world of positive inflation, nominal interest rates sit higher than they would in a zero-inflation environment, which gives the Federal Open Market Committee actual space to cut when a recession hits. If the baseline sat at 0%, the economy would slam into the zero lower bound almost immediately during a downturn, forcing central banks into more experimental territory - quantitative easing, negative rates, the kind of tools that spook markets. Aiming for 2% keeps a lever available for when the credit cycle inevitably turns.

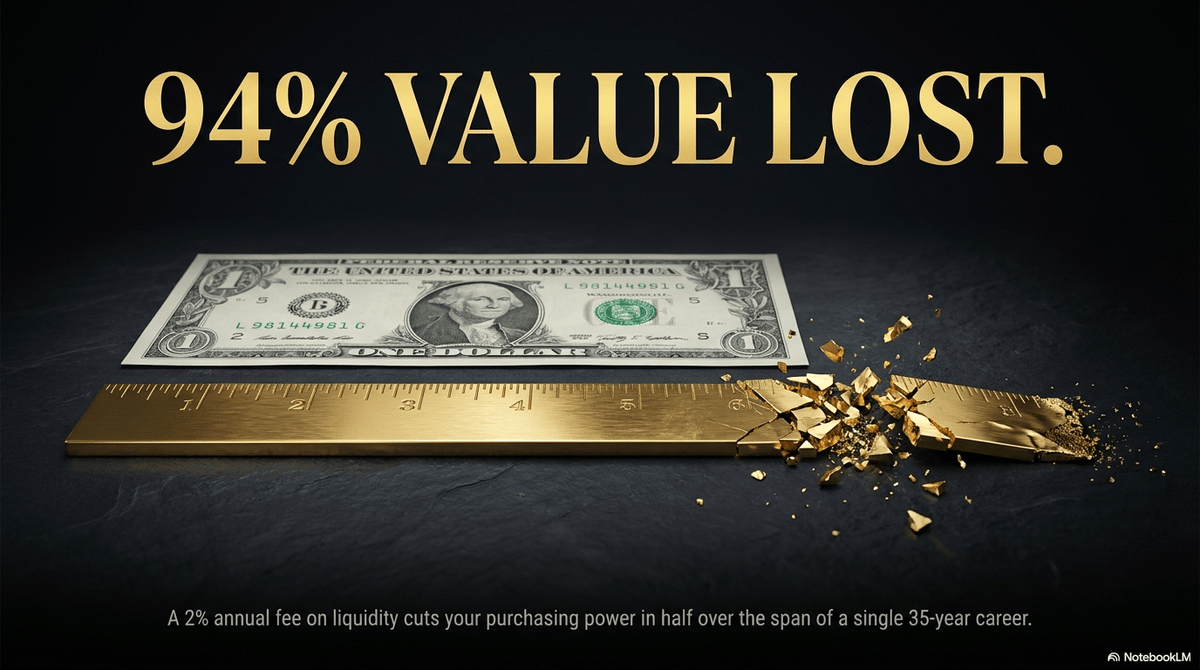

The cost of that flexibility, though, is borne entirely by whoever holds the currency. A 2% annual loss sounds trivial on paper. The compounding effect is not. Over roughly 35 years - the span of a single career - the purchasing power of static savings gets cut in half. Extend the timeline and the math turns brutal: based on Bureau of Labor Statistics CPI data, a dollar in 1924 buys roughly what $18 buys today, a loss of value north of 94%. That's not a system failure. That's the system doing exactly what it was built to do.

Gold as the scarcity counterweight

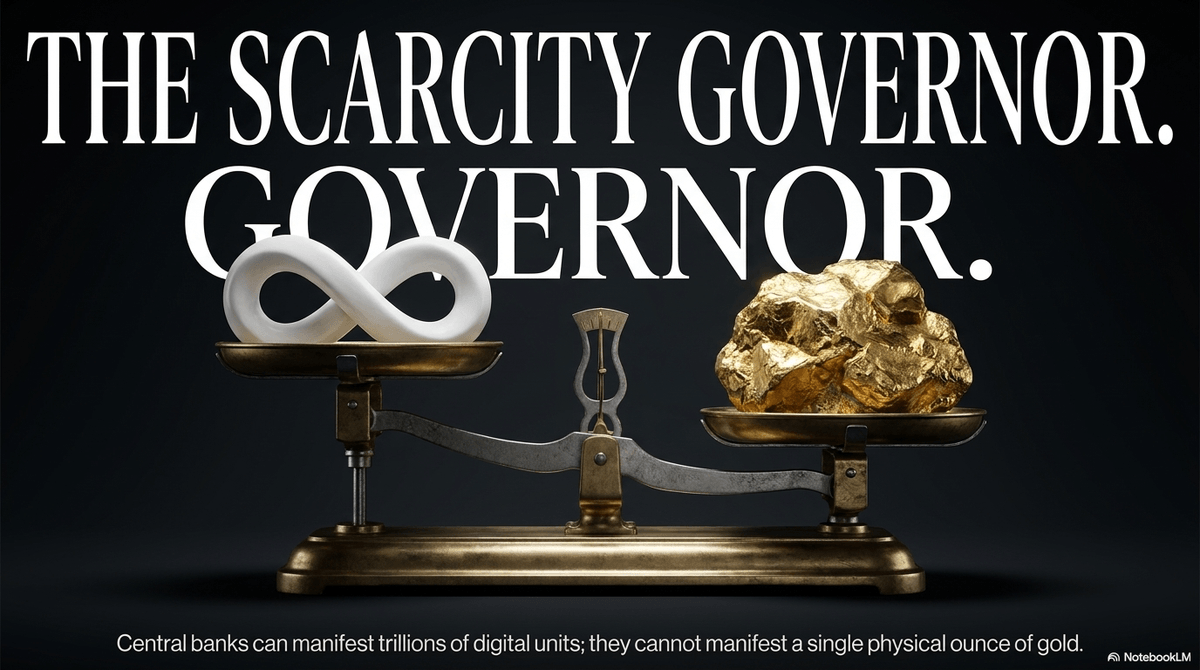

The fundamental split between fiat and gold comes down to elasticity of supply. Fiat currency is backed by government decree and the full faith and credit of the issuing nation, and its supply is limited only by a central bank's willingness to expand its balance sheet. Gold is a physical commodity that takes real energy and capital to extract. Global mine supply grows at a slow, predictable rate of roughly 1-2% a year, and that pace has stayed remarkably flat even as prices have surged to record highs - which tells you supply doesn't chase price the way you'd expect from an ordinary commodity.

That physical constraint acts as a natural governor on the system. A central bank can create a trillion units of currency with a digital keystroke. A mining company cannot manifest a trillion ounces of gold, full stop. This scarcity is why gold has functioned as a store of value for millennia. It pays no dividend, carries no yield, and still tends to outperform fiat over long stretches precisely because it can't be debased at the whim of a fiscal authority staring down a budget deficit.

In the current cycle, gold has become shorthand for what traders call the "debasement trade" - capital rotating out of sovereign debt and cash and into hard assets when investors expect heavy government borrowing and central bank monetization of that debt. As long as the policy goal remains a 2% annual reduction in currency value, the incentive to hold a fixed-supply asset never really goes away.

If you want to see the debasement trade in real time, look at who's been buying. Central banks have kept adding to reserves at a pace that would have seemed extreme a decade ago - Poland's central bank alone accumulated over 60 tonnes in the first five months of 2026, working toward a long-stated 700-tonne target. Official-sector buying has averaged roughly 1,000 tonnes a year over the past four years, double the pace of the prior decade, and the large majority of surveyed reserve managers expect global official holdings to keep climbing through 2027. That's not retail speculation. That's sovereign institutions making a multi-year bet against their own currency exposure.

The 1971 shift and the end of convertibility

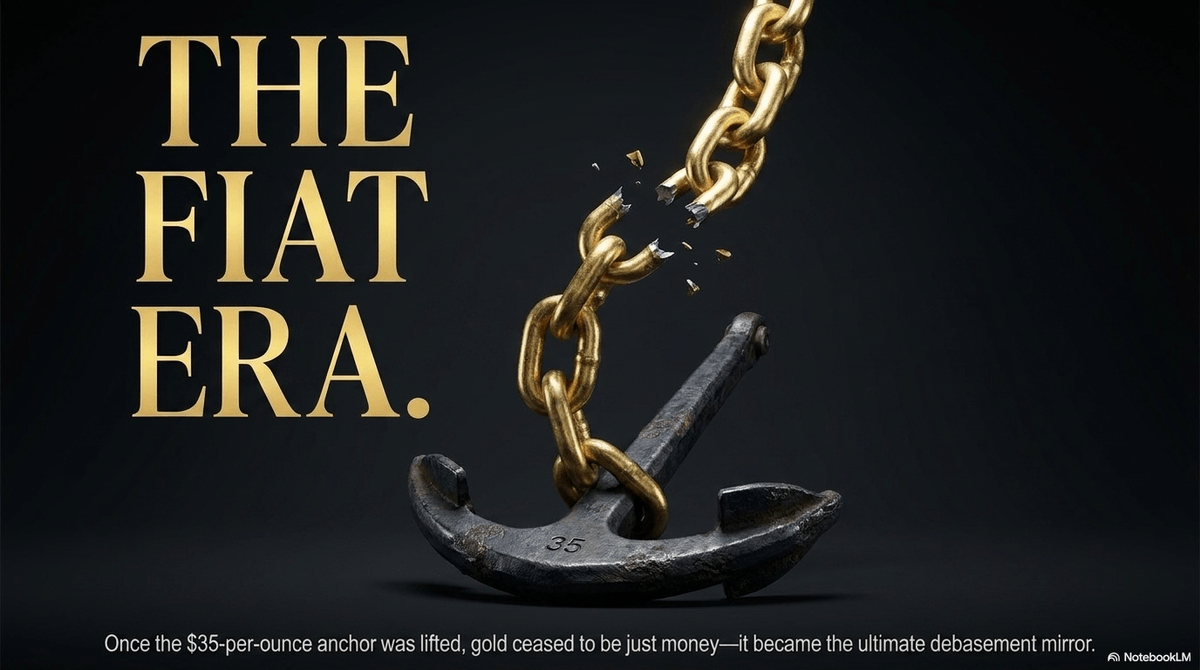

To understand the modern divergence, you have to go back to the fracture point of 1971. Before that year, the Bretton Woods system tied the U.S. dollar to gold at $35 an ounce, which put a hard cap on how far the money supply could expand. When President Richard Nixon suspended dollar-to-gold convertibility, the world entered a pure fiat era, and the results over the following decades have been stark.

Since 1971, the dollar has lost somewhere in the neighborhood of 87-88% of its purchasing power on a CPI basis - the exact figure moves depending on the calculation window, but every credible estimate lands in that range. Gold, over the same period, has moved from $35 an ounce to trading above $4,100 as of mid-2026, after briefly touching an intraday all-time high above $5,600 in January 2026. That's not gold "becoming more valuable" in some abstract sense. It's gold reflecting the systematic devaluation of the currency it's priced in. Gold acts as a mirror. When the paper yardstick shrinks, the nominal price stamped on the gold bar simply grows to match.

This history matters because it shows the gold standard era - where inflation averaged closer to zero over long stretches - was a genuinely different animal. It had its own short-term volatility, no argument there, but it preserved long-term purchasing power in a way the fiat system was never designed to do. The fiat system inverted that trade-off entirely: short-term price "stability" via the 2% crawl, purchased at the cost of long-term value destruction. For anyone thinking in multi-generational terms about wealth, that trade-off is worth sitting with.

Safe haven demand and the dollar's inverse pull

Gold's divergence from fiat is also driven by its role as a safe haven asset. A bank deposit is a promise from a financial institution. A dollar bill is a promise from a government. Gold is neither - it isn't anyone's liability, which is precisely why markets assign it a premium during periods of geopolitical instability or systemic banking stress. This is why gold prices tend to spike during periods of heightened international tension, financial crises, or extreme volatility. The World Gold Council's most recent survey of central bank reserve managers found that performance during times of crisis was the single most-cited reason for holding gold, ahead of long-term store of value and portfolio diversification.

Gold also carries a fairly reliable inverse relationship with the U.S. dollar. Because gold is priced globally in dollars, a weaker dollar - whether from low rates or aggressive money creation - makes gold cheaper for holders of other currencies, which pulls in more demand. That creates a feedback loop: as the dollar gets debased to hit the 2% target, gold becomes more attractive, which pulls capital further away from the currency being managed in the first place.

There's a structural angle here too. The freezing of a significant share of one major central bank's foreign reserves in 2022, in response to geopolitical events, signaled to reserve managers everywhere that dollar-denominated holdings aren't unconditionally insulated from sanctions risk. That event appears to have accelerated a multi-year shift: gold now accounts for a larger share of global central bank reserves than U.S. Treasuries for the first time since 1996, a milestone that says a great deal about how reserve managers are rethinking counterparty risk in the current environment.

Fiscal stress and the abandonment of stability

Some economists argue a fiat system could, in theory, achieve durable price stability if the central bank stays genuinely independent and sticks to its mandate. In practice, the fiscal stress of modern governments tends to make that independence a polite fiction. When governments run large deficits, they lean on the central bank to keep rates low enough that the debt stays serviceable.

That produces financial repression - interest rates held below the inflation rate, which means savers lose money in real terms every single day their capital sits in a bank account. Gold thrives in exactly this environment. It has no interest rate for a central bank to suppress, which makes it the natural refuge for capital trying to escape negative real rates.

The pattern that stands out across recent gold market research: sovereign buyers keep accumulating even as prices sit near record highs, which points to long-term strategic positioning rather than short-term speculation.

That's the tell. When institutional buyers with multi-decade horizons keep accumulating at record prices, they're not chasing a trade. They're hedging a currency regime.

Strategic implications for wealth preservation

For the professional investor, the 2% inflation target isn't a signal to relax. It's a signal to hedge. Protecting purchasing power in a fiat-dominant world starts with understanding the currency debasement floor and building around it deliberately.

- Asset allocation. Diversifying away from pure cash and fixed income into hard assets - gold, silver, select real estate - can offset the drag of the 2% crawl over time.

- Real returns versus nominal returns. Always net out the inflation rate before calling something a gain. A 4% return against 2% inflation is a 2% real gain, full stop. When currency debasement runs hotter than the stated target, which happens more often than the official narrative admits, nominal gains can quietly become real losses.

- Watch the balance sheet, not just the headline number. The gold-fiat divergence tends to widen most aggressively when central bank balance sheets are expanding. Tracking M2 money supply growth gives a more forward-looking read on future debasement than the consumer price index alone, since CPI tends to lag the underlying monetary expansion by months or years.

- Size the position to the thesis, not the headline. Gold's role in a portfolio is insurance against currency debasement, not a replacement for productive, yield-bearing assets. Treat it accordingly.

If you're trying to separate structural demand from short-term noise, it helps to understand how inflation expectations shape what we pay in the first place - because a large part of gold's price action is investors pricing in future debasement before it shows up in the official data.

The long-term divergence outlook

Looking ahead, the forces pulling gold and fiat apart show no sign of reversing. Global debt-to-GDP ratios keep climbing, and the political appetite for genuine austerity is close to nonexistent in most major economies. That points toward central banks remaining lenders of last resort indefinitely, with the 2% inflation target serving as the floor rather than the ceiling for acceptable debasement. Some analysts have floated scenarios where central banks quietly tolerate a 3% or 4% target to help inflate away accumulated sovereign debt loads - a move that would only widen the gap gold is pricing in.

Major bank forecasters have leaned into that thesis. J.P. Morgan Global Research has projected gold pushing toward $6,000 an ounce by year end, with $6,300 seen as plausible for the following year. The bank has also flagged the main risk to that call: a scenario where inflation keeps accelerating while growth and employment stay resilient, which could embolden the Fed to keep rates higher for longer and eventually crack investor demand for a non-yielding asset. That's a fair caveat, and it's worth remembering gold doesn't move in a straight line - the metal corrected roughly 25% off its January 2026 intraday peak before stabilizing, a reminder that "structural uptrend" and "smooth ride" are not the same thing.

Gold, by its nature, resists policy maneuvering in a way paper currency simply can't. It remains a core holding for anyone who recognizes that "price stability," in practice, is often a polite way of describing predictable devaluation. The divergence between hard assets and fiat currency is the continuation of a trend that started the moment the world cut its last tie to hard money. As long as monetary expansion stays the primary tool for economic management, gold will keep functioning as the floor beneath which wealth preservation gets measured.

Share now

Key takeaways

- Central banks, including the Federal Reserve and European Central Bank, target roughly 2% annual inflation to avoid deflation risk and preserve room to cut rates during downturns.

- The 2% target traces back to an offhand 1988 New Zealand television interview, later formalized into policy - it was never derived from rigorous empirical modeling.

- At a steady 2% annual debasement rate, currency purchasing power halves roughly every 35 years.

- Based on Bureau of Labor Statistics CPI data, a 1924 dollar buys about what $18 buys today - a purchasing power loss of roughly 94%.

- Since the 1971 end of dollar-gold convertibility (the "Nixon Shock"), the dollar has lost an estimated 87-88% of its purchasing power on a CPI basis.

- Gold has risen from $35 an ounce in 1971 to trading above $4,100 by mid-2026, after briefly touching an intraday all-time high above $5,600 in January 2026.

- Global gold mine supply grows at a slow, predictable 1-2% annually, a physical constraint fiat currency doesn't share.

- Central banks have purchased an average of roughly 1,000 tonnes of gold per year over the past four years, double the prior decade's pace.

- Poland has been among the most aggressive sovereign buyers in 2026, working toward a stated 700-tonne reserve target.

- Gold now represents a larger share of global central bank reserves than U.S. Treasuries for the first time since 1996.

- The "debasement trade" describes capital rotating from sovereign debt and cash into hard assets when investors anticipate heavy government borrowing and monetary expansion.

- Financial repression - interest rates held below the inflation rate - erodes saver purchasing power daily and tends to boost gold's relative appeal since it carries no suppressible yield.

Sources

- World Gold Council https://www.gold.org/goldhub/research/central-bank-gold-reserves-survey-2026

- Bank of Canada https://www.bankofcanada.ca/2025/09/why-we-target-2-inflation/

- U.S. Bureau of Labor Statistics (via WPUNJ analysis) https://online.wpunj.edu/degrees/business/mba/general/impact-inflation-on-purchasing-power/

- Schwab https://www.schwab.com/learn/story/understanding-debasement-trade

- J.P. Morgan Global Research https://www.jpmorgan.com/insights/global-research/commodities/gold-prices

- Published 2026-07-19 09:35

- Modified 2026-07-19 09:35

-

Redaction