-

Redaction

Redaction

Emergency fund: How much do you really need?

An exhaustive analysis of emergency fund strategies, liquidity requirements, and the macroeconomic impact of household savings in a volatile global economy.

The fundamental necessity of liquidity buffers

Economic stability is rarely a static condition. For the individual participant in the modern market, financial survival depends less on gross income and more on the presence of a dedicated liquidity buffer. An emergency fund - sometimes called a rainy day fund, cash reserve, or financial cushion - is a specialized savings vehicle designed specifically to offset the impact of unforeseen expenditures or systemic income disruptions.

It functions as a primary defensive layer, ensuring that a temporary shock does not evolve into a permanent fiscal collapse. In a landscape characterized by asymmetric risks, the utility of liquid capital cannot be overstated. It provides the necessary friction against the gravitational pull of high-interest debt cycles.

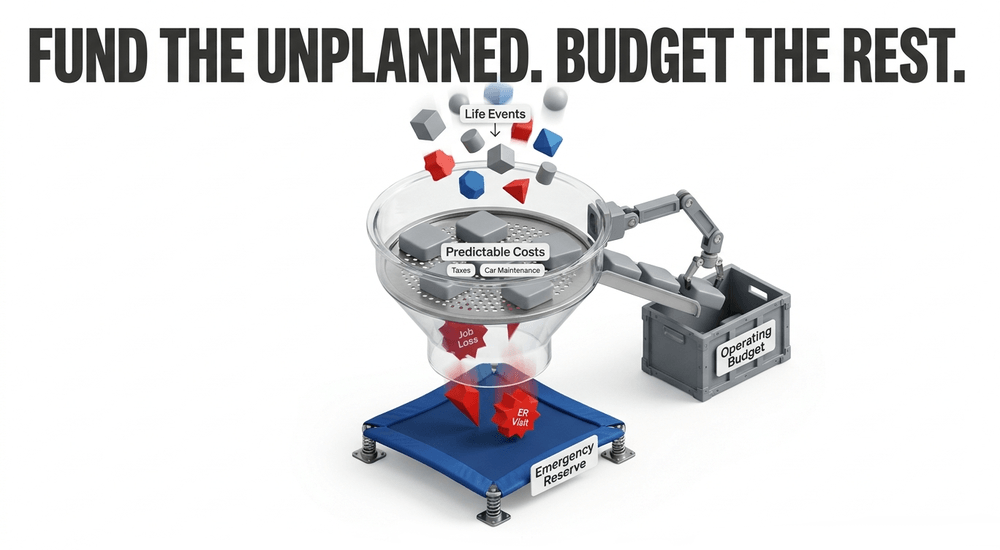

Defining the scope of emergency capital

Not every unexpected cost qualifies as a true emergency - and that distinction matters more than most people realize.

A true emergency is an event that is both unplanned and urgent. This includes sudden medical requirements, involuntary loss of employment, or catastrophic failures in essential infrastructure, such as a primary vehicle or home heating system. Conversely, predictable costs like annual tax obligations or routine car maintenance should be integrated into a standard operating budget rather than drawn from an emergency reserve.

By maintaining this distinction, an individual preserves the integrity of their safety net for high-impact, low-probability events - precisely the scenarios where no alternative funding source exists.

How much should your emergency fund actually be?

Calculations for emergency reserves are frequently oversimplified into a single number. A data-driven approach, however, requires a more granular analysis of cash flow and risk exposure. While the general consensus among financial experts suggests three to six months of essential living expenses, this figure serves only as a starting point. The specific requirements of a household are dictated by its unique liability profile and the volatility of its revenue streams.

Income stability and sector volatility

Revenue consistency is the single most significant variable in determining the right fund size.

Historical employment data consistently shows that individuals operating in cyclical industries - or those with 1099 income structures - face longer periods of unemployment between contracts than salaried workers. For a government employee with high job security and predictable income, a three-month buffer may be entirely sufficient.

In contrast, a freelance consultant, gig worker, or small business owner in a volatile sector should target a twelve-month reserve. This larger cushion accounts for the time required to secure new revenue streams in a depressed labor market, where the search period itself can stretch considerably longer than average.

Essential vs. discretionary expenditures

Precision in budgeting is required to calculate the true "burn rate" during a crisis. The target amount must be based on essential expenses only, not current lifestyle spending.

Non-negotiable costs include:

- Housing (rent or mortgage)

- Utilities and internet

- Basic groceries and household essentials

- Transportation (loan payments, insurance, fuel)

- Minimum debt servicing obligations

- Insurance premiums

Insurance premiums deserve particular attention. Allowing coverage to lapse during an emergency introduces unmanageable secondary liability - precisely when financial exposure is already at its highest. Discretionary spending such as entertainment, dining out, and subscription services is excluded from these calculations on the assumption that these costs would be immediately suspended during a genuine financial shock.

The impact of dependents and health risks

Risk increases proportionally with the number of dependents. Households with children or elderly relatives require larger buffers to account for the increased probability of medical emergencies or childcare disruptions - two costs that rarely arrive on a convenient schedule.

Health considerations also play a vital role. If a household member has a chronic condition, the emergency fund must be large enough to cover insurance deductibles and out-of-pocket maximums without exhausting the reserve before the end of a single fiscal year. In practical terms, this often means the fund needs to be sized to absorb the family's full annual out-of-pocket maximum in a worst-case scenario.

Geographic and environmental risk factors

Modern financial planning must also account for location-specific risks. For individuals living in regions prone to natural disasters - hurricane corridors, seismic zones, or flood plains - the standard three-to-six-month rule may prove dangerously insufficient.

Evacuation costs, insurance deductibles for property damage, and temporary housing are significant expenses that frequently arrive simultaneously. In these contexts, the emergency fund must be scaled to cover the specific deductibles outlined in homeowner and flood insurance policies, in addition to the standard income-replacement buffer.

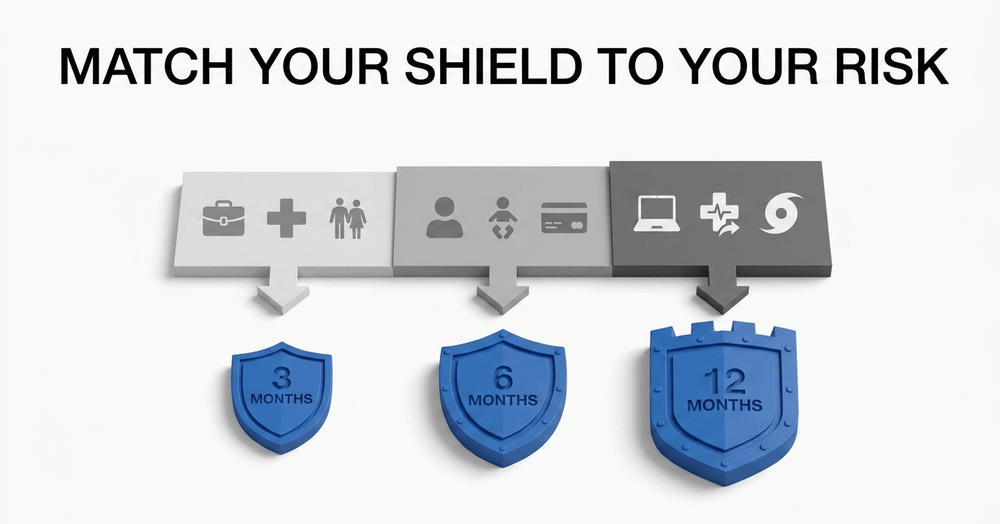

A practical framework: matching your fund to your risk profile

Rather than treating the "three to six months" rule as universal, consider your position across these three dimensions:

Lower risk profile (3 months may suffice): Stable salaried employment in a recession-resistant sector, dual income household, no dependents, comprehensive health coverage, low personal debt, and no known major expense on the horizon.

Moderate risk profile (6 months recommended): Single income household, moderately volatile employment, at least one dependent, moderate health or property risk, or significant outstanding debt.

Higher risk profile (9-12 months advised): Self-employed or freelance income, single income with multiple dependents, chronic health condition in the household, geographic exposure to natural disasters, or a recent history of income disruption.

This framework is not a substitute for personalized financial advice, but it provides a more honest starting point than a single number applied to every household.

The macroeconomic reality of household savings

The gap between financial theory and consumer reality remains stark - and the data from recent years makes that clear.

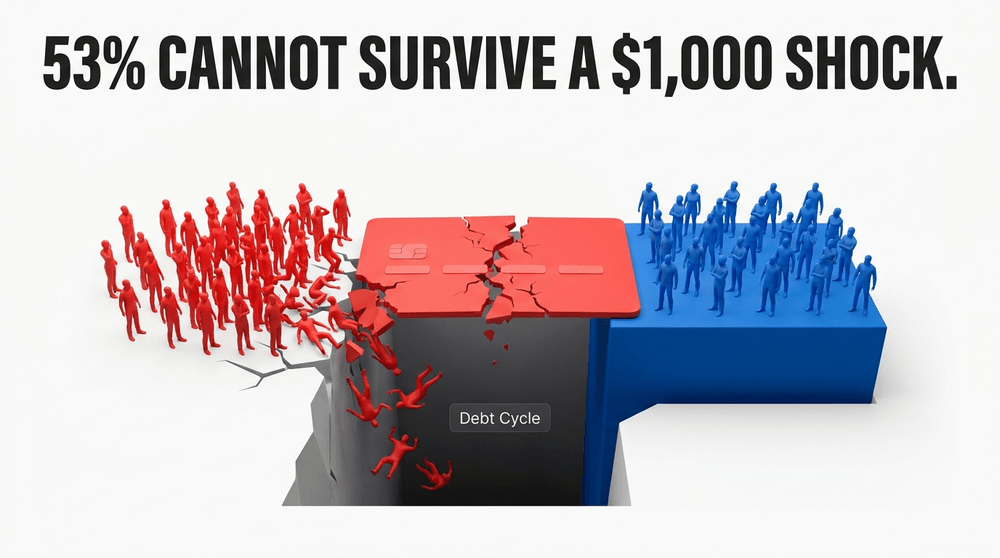

A Bankrate Emergency Savings Report, based on a survey conducted in late 2025, found that only 47% of Americans indicate they have sufficient liquidity or access to funds to cover a $1,000 emergency expense. That means 53% of American adults cannot cover a $1,000 emergency without going into debt.

A separate Bankrate study, based on surveys conducted in early 2025, found that 33% of Americans have more credit card debt than emergency savings - meaning that for roughly one in three households, any unexpected expense deepens an already-negative net worth position.

The Federal Reserve's Survey of Household Economics and Decisionmaking (SHED), covering 2024, found that 37% of adults would not cover an unexpected $400 expense with cash or its equivalent, and a striking 13% of all adults said they would be unable to pay such an expense by any means.

These statistics highlight a systemic vulnerability. When a significant portion of the population relies on debt to manage minor shocks, the broader economy becomes more susceptible to recessionary pressures. Debt accumulated during a crisis compounds the original problem, as high interest rates redirect future income toward debt service rather than consumption or investment.

Strategic advantages of a liquid cash reserve

Beyond simple survival, a robust emergency fund provides strategic flexibility. In financial terms, this is often referred to as optionality - the ability to make decisions based on long-term value rather than short-term desperation.

Preventing debt cycles

Reliance on high-interest credit cards is the primary cause of long-term financial decay. When an emergency is financed through credit, the total cost of that emergency increases by the effective interest rate of the debt - often 20% or more annually. An emergency fund breaks this cycle entirely by providing zero-interest capital for repairs, medical bills, or income gaps.

Protecting long-term investments

Without a liquid buffer, individuals are often forced to liquidate long-term assets - retirement accounts, brokerage positions, or home equity - during market downturns. This forced selling typically occurs at suboptimal prices and may trigger significant tax penalties or the permanent loss of future compounded growth.

An emergency fund acts as a firewall protecting the retirement portfolio from the volatility of daily life. The ability to leave long-term investments untouched during a two- or three-month income disruption can make a measurable difference to final retirement outcomes.

Psychological and physical health outcomes

The correlation between financial security and physical health is well-documented in peer-reviewed research. Studies published in the National Institutes of Health literature indicate that financial instability is associated with chronic illness, elevated stress hormones, and reduced mental health outcomes across all age groups.

Children living in households with less than three months of savings face a statistically higher risk of obesity and related health complications, according to published research. The peace of mind provided by an adequate safety net is not merely a subjective feeling - it is a measurable benefit to long-term physical well-being.

Where to keep your emergency fund

The location of an emergency fund is as important as its size. The primary objectives for these funds are liquidity and capital preservation - not yield maximization. Consequently, the assets must be held in vehicles that allow for immediate access without the risk of principal loss.

High-yield savings and money market accounts

These accounts are the most efficient tools for holding emergency capital in 2026. They offer competitive interest rates while maintaining FDIC or NCUA insurance, ensuring the principal is fully protected up to applicable limits.

Unlike certificates of deposit (CDs), these accounts do not typically penalize early withdrawals, making them ideal for the unpredictable nature of emergencies. A practical recommendation: keep these funds in a separate institution from your primary checking account. The slight friction of a transfer creates a meaningful psychological barrier against using the money for non-emergencies.

The risks of volatile assets

Investing emergency funds in the stock market or cryptocurrency is a fundamental strategic error - not a matter of opinion, but of timing risk.

If an emergency coincides with a market correction, the value of the safety net could be reduced by 20% to 50% at the exact moment it is needed most. The so-called opportunity cost of keeping money in a high-yield savings account is simply the premium one pays for the insurance of having capital available on demand. That is not a cost to be minimized - it is the entire point.

How to build your emergency fund from zero

Constructing a fund from zero requires a systematic approach. Expecting to accumulate six months of expenses rapidly is unrealistic for most households. Instead, the process should be viewed as a series of incremental milestones, each building momentum for the next.

Start with a $1,000 starter fund

The first objective should be a starter fund of $1,000. This amount is sufficient to cover the most common minor financial shocks - a tire replacement, a basic medical co-pay, or an unexpected utility bill. Once this baseline is established, the focus shifts to reaching the one-month expense mark.

Achieving these smaller goals builds the psychological momentum necessary to maintain long-term saving habits. The behavioral dimension of saving is often underestimated; progress that is visible and measurable sustains effort far more effectively than abstract long-term goals.

Automate everything

Manual saving is prone to human error and emotional decision-making. The most effective method for building a reserve is automation. By scheduling a direct transfer from each paycheck to the savings account on payday, the individual treats the emergency fund as a mandatory expense - not an optional surplus.

This "pay yourself first" strategy ensures that savings occur before discretionary spending is possible, removing willpower from the equation entirely.

Review and replenish regularly

An emergency fund is not a static asset. As life circumstances evolve, so do financial requirements. A promotion, the birth of a child, the purchase of a home, or a significant increase in monthly obligations all necessitate an upward revision of the fund's target.

Furthermore, if the fund is utilized, it must be replenished with the same urgency as the initial build. The period immediately following an emergency is often the most financially vulnerable window for a household - the buffer has been depleted, but the statistical likelihood of a secondary shock remains elevated.

Frequently asked questions about emergency funds

Can I count my credit card limit as part of my emergency fund? No. A credit line is debt capacity, not savings. Using it in an emergency creates an interest-bearing obligation that compounds the original problem. A true emergency fund is cash or its equivalent - accessible without creating new liability.

Should I invest my emergency fund to beat inflation? No. The purpose of an emergency fund is availability, not growth. The cost of holding cash in a high-yield account is the price of insurance - the same reason you don't question your home insurance premium. Keep the fund liquid, insured, and separate from investment accounts.

What if I have high-interest debt? Should I pay that off first or build an emergency fund? Build the starter $1,000 fund first, then focus aggressively on high-interest debt. Without any buffer, a minor unexpected expense will send you straight back to that credit card anyway. Once high-interest debt is cleared, redirect those payments into building the full reserve.

Is a joint emergency fund appropriate for couples? Yes - in most cases, a combined household fund is more efficient. However, both partners should be aware of the fund's location, current balance, and withdrawal process. In households with significantly different risk profiles (for example, one self-employed, one salaried), consider sizing the fund based on the higher risk profile.

Conclusion: The fire extinguisher analogy

The utility of an emergency fund is best understood through the analogy of a fire extinguisher. It occupies space and offers no daily benefit - yet its presence is non-negotiable. Its value is realized only during a crisis, at which point its absence is catastrophic.

In an increasingly complex and volatile global economy, the maintenance of a liquid cash reserve is the hallmark of sound financial management. It is the bridge between a temporary setback and a permanent disaster, providing the stability required to pursue long-term prosperity without the constant threat of insolvency.

The goal is not perfection. It is progress. A $1,000 starter fund is meaningfully better than nothing. Three months is better than one. The most important step is always the next one.

Share now

Key takeaways

- Financial experts recommend three to six months of essential living expenses as a baseline emergency fund target, with higher-risk earners - freelancers, self-employed individuals, and those in volatile sectors - advised to target up to twelve months.

- A Bankrate Emergency Savings Report (late 2025) found that 53% of Americans lack sufficient liquidity or access to funds to cover a $1,000 emergency expense without going into debt.

- Approximately one in three Americans holds more credit card debt than emergency savings, according to Bankrate research - meaning any unexpected expense deepens an already-negative net worth position.

- The Federal Reserve's Survey of Household Economics and Decisionmaking (SHED, 2024) found that 37% of adults would not cover an unexpected $400 expense with cash or its equivalent, and 13% of all adults said they would be unable to pay such an expense by any means.

- High-yield savings accounts and money market accounts are the preferred vehicles for emergency capital due to their full liquidity, FDIC or NCUA deposit insurance, and absence of early-withdrawal penalties.

- Research published via the NIH shows that children in households with less than three months of savings face a statistically elevated risk of obesity and other adverse health outcomes - demonstrating that the impact of financial instability extends well beyond finances.

- Keeping an emergency fund in a separate institution from your primary checking account reduces the temptation to use the reserve for non-emergency spending - a behaviorally significant factor in fund preservation.

- Investing emergency reserves in stocks or cryptocurrency is considered a fundamental strategic error: if an emergency coincides with a market downturn, the fund's value could decline 20-50% at the exact moment it is needed most.

Sources

- Bankrate - Emergency Savings Report https://www.bankrate.com/banking/savings/emergency-savings-report/

- Federal Reserve - Report on the Economic Well-Being of U.S. Households, SHED 2024 https://www.federalreserve.gov/publications/2025-economic-well-being-of-us-households-in-2024-savings-and-investments.htm

- Vanguard - Emergency fund guidance https://investor.vanguard.com/investor-resources-education/emergency-fund

- Experian - Do you really need to save three to six months of expenses? https://www.experian.com/blogs/ask-experian/do-you-really-need-to-save-three-to-six-months-worth-of-expenses/

- NIH / PubMed Central - Financial hardship and health outcomes https://pmc.ncbi.nlm.nih.gov/articles/PMC7236434/

- Chase - How much should I have in an emergency fund? https://www.chase.com/personal/banking/education/budgeting-saving/how-much-should-i-have-in-emergency-fund

- Published 2026-05-27 13:33

- Modified 2026-05-27 13:33