-

Redaction

Redaction

The OBBBA fiscal audit: what the deficit hides

The 'Beautiful Bill' promised prosperity, but retroactive tax fixes created a $4.7 trillion hole. An audit separating real cost from deficit-headline noise.

The fiscal reality of 2026 is not a product of current economic performance. It is a ghost of legislation past, and the paperwork is only now coming due.

The One Big Beautiful Bill Act (OBBBA) was signed into law promising a new era of American prosperity through aggressive tax restructuring. On paper, the federal ledger looks almost stable: the deficit through the first eight months of this fiscal year actually came in lower than the same period last year. But that headline number is doing a lot of work to hide what is happening underneath it.

This audit looks past the top-line figure to the mechanism the law actually built: a retroactive tax architecture that let corporations and high-net-worth households reach back into 2022, 2023, and 2024 and pull money out of years that had already closed. The bill for that architecture is not fully written yet. The Congressional Budget Office puts the ten-year cost at $4.7 trillion. That is the number that matters, not the monthly noise.

If your organization is affected by any of the provisions discussed here, the IRS newsroom and the Taxpayer Advocate's public reports are the most current primary sources, and a licensed tax professional can walk through what applies to your specific filings.

The $4.7 trillion question

Start with the nonpartisan number, because everything else in this story hangs off it. CBO estimates that OBBBA will increase deficits by $4.7 trillion over 10 years, a dynamic estimate that folds in both interest costs and the law's broader effects on the economy. Break that down and the law is projected to reduce revenue by $4.9 trillion, reduce spending by $1.2 trillion, and increase interest costs by over $850 billion across the 2026-through-2035 budget window. Some of that cost is offset elsewhere in fiscal policy, mostly by tariff revenue, but the tax law itself stands as the largest single driver of the coming decade's deficits, responsible for just over one-fifth of total projected deficits through 2035.

That is a debt commitment on a scale most legislation never approaches. For comparison, it makes OBBBA the most expensive law passed by Congress since the 2012 American Taxpayer Relief Act, which was itself a $4 trillion measure. The difference is that the 2012 law didn't reach backward into years that had already closed their books.

What the deficit numbers actually show

Here is where an honest audit has to correct the record. The federal deficit through the first eight months of fiscal year 2026 totaled $1.2 trillion, and that figure is not a sign of a revenue collapse. It's the opposite. Treasury data shows the FY2026 deficit running $118 billion, or 9 percent, below the cumulative FY2025 deficit, driven by $174 billion of higher revenue collections against a modest rise in spending.

That improvement, though, is not evenly distributed, and this is where OBBBA's retroactive provisions actually show up in the ledger. Corporate income tax receipts fell $88 billion, a 30 percent drop, largely attributable to OBBBA's business tax changes, including the larger deductions now available for certain business investments. That decline sits inside a deficit picture that is otherwise improving, propped up by strong individual income and payroll tax collections. It is a split ledger: individuals paying in more, corporations claiming back more, and the retroactive R&E fix is a meaningful part of why.

There's a second factor muddying the picture that has nothing to do with OBBBA at all, and any honest accounting needs to separate it out. In February 2026, the Supreme Court ruled that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unconstitutional, and the government began refunding an estimated $166 billion to roughly 330,000 importers. That refund wave is a major reason customs duty collections declined drastically in May, and it is a wholly separate legal and fiscal event from the tax law. Conflating the two would be sloppy. The OBBBA drain is real. It is just smaller, so far, than the raw deficit headline suggests, and it is running alongside an unrelated tariff unwind that is muddying the same monthly data.

The retroactive drain: Section 174 and the R&E fix

The most legally distinctive piece of OBBBA, and the one that most directly created a "reach back and reclaim" dynamic, is the permanent reinstatement of full expensing for domestic Research and Experimentation (R&E) costs under new Section 174A. Previous rules forced businesses to amortize these expenses over five years. OBBBA didn't just end that rule going forward. It let certain businesses undo it retroactively.

Small businesses with average gross receipts under $31 million were granted the ability to retroactively apply Section 174A to domestic R&E expenditures paid or incurred in tax years beginning after December 31, 2021, meaning 2022, 2023, and 2024 returns could be reopened and amended. The deadline for making that election closed on July 6, 2026, one year to the day after enactment, and by all accounts tax professionals spent the run-up to that deadline filing amended returns at volume, racing a hard statutory cutoff with no extensions available.

For larger businesses above the $31 million threshold, the retroactive door was never open. Instead, OBBBA gave them a one-time acceleration option: firms could recover any remaining unamortized 2022-through-2024 domestic R&E expenses entirely in 2025, or split the recovery between 2025 and 2026. Every firm that chose the 2026 split, likely to offset income they expect to be higher this year, pushed a chunk of the fiscal cost squarely into the current filing season.

- Small businesses (under $31 million in average gross receipts): could amend 2022-2024 returns directly, deadline July 6, 2026

- Larger businesses: no retroactive amendment option, but could accelerate unamortized balances into 2025, or split the recovery across 2025 and 2026

- Foreign R&E expenditures: unaffected by any of this, still amortized over 15 years under the original Section 174

This is not a fringe provision. It touches nearly any business that spent money on U.S.-based software development, engineering, or product research over the past three years, which is a lot of companies.

Individual retroactivity and the SALT cap shift

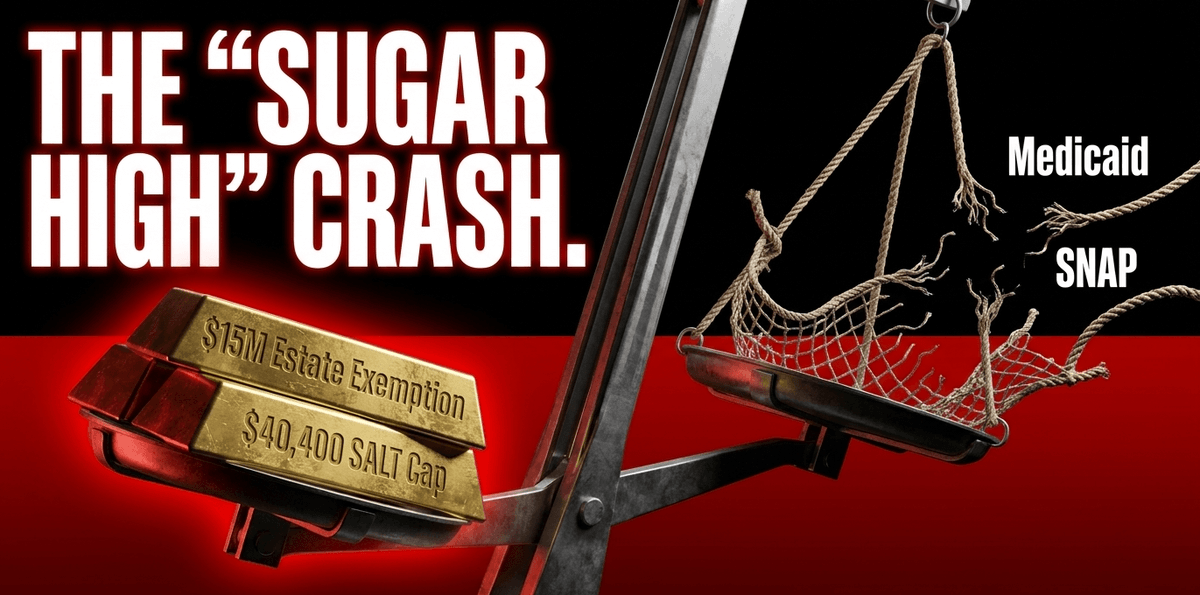

The corporate sector isn't carrying this alone. OBBBA applied a similar retroactive logic to individual deductions, most visibly through the state and local tax (SALT) cap. The cap was raised, retroactively, to $40,000 for the 2025 tax year, up from the $10,000 ceiling that had been in place since the 2017 Tax Cuts and Jobs Act. Because those benefits are being claimed on returns filed during the current filing season, the cash-flow effect lands squarely in 2026, not 2025, when the law was actually signed.

For 2026 itself, the cap climbs again, to roughly $40,400, with a phase-down that reduces the benefit for taxpayers whose modified adjusted gross income exceeds $500,500. The reduction cannot push the deduction below a $10,000 floor. The math here rewards a fairly narrow band of upper-middle to high earners in high-tax states; taxpayers well above the phase-out range see little practical change from the cap increase at all.

None of this is temporary in the way the tips or overtime deductions are. The SALT cap increase runs through 2029, then reverts to $10,000 in 2030 absent further Congressional action, setting up a cliff that will likely dominate tax headlines the way the original TCJA sunset did in 2025.

Operational collapse: the IRS under siege

While the law generates a wave of amended returns and new elections, the agency responsible for processing all of it has been hollowed out. The IRS started 2025 with about 102,000 employees and finished with about 74,000, a reduction of 27 percent, according to the National Taxpayer Advocate's annual report to Congress. That reduction hit essentially every corner of the agency, and it landed at the worst possible moment: entering a filing season defined by more than 100 tax code changes, many of them retroactive, on top of leadership turnover that saw the agency cycle through seven commissioners and acting commissioners over the course of a year.

The consequences are not abstract. The Budget Lab at Yale projects that the 2025 staffing reductions alone will reduce IRS revenues by almost $600 billion over the 2026-2035 budget window, driven not by fewer salaries paid out but by fewer audits conducted and less enforcement capacity generally. By mid-2025, the agency had already lost more than 3,600 revenue agents, roughly 31 percent of its entire auditing staff, the employees responsible for the complex examinations of high-income individual returns, partnerships, and large corporations that yield the most revenue per audit hour. Cutting there does not save money. It defers collection, and often forfeits it entirely once the statute of limitations runs out.

That matters even more given what the IRS actually does. The agency is the mechanism through which the federal government collects 96 percent of its revenues. Treating it as an ordinary line item for budget cuts misreads what it is: not a cost center, but the collection arm without which none of the rest of the budget functions.

None of this is happening on paper alone, either. The Government Accountability Office found that as the agency prepared to implement OBBBA, an internal IRS report stated that critical technology systems would not be ready in time for the start of the 2026 filing season. The Taxpayer Advocate's own read on the situation is blunt: entering 2026, the agency faces a reduction of 27 percent of its workforce, leadership turnover, and the implementation of extensive and complex tax law changes, many of them retroactive, all at once.

The estate tax and the $15 million exemption

Further out on the timeline, OBBBA's treatment of estate taxes tells its own story about who the law was built for. The federal estate, gift, and generation-skipping transfer tax exemption rose to $15 million per person, or $30 million for a married couple, effective January 1, 2026, and unlike most of the law's individual provisions, this one does not sunset. It's permanent, and it will be indexed for inflation starting in 2027.

To put that in context: without OBBBA, the exemption was on track to roughly halve at the start of 2026 under the original TCJA sunset schedule. Instead, Congress not only prevented the drop, it raised the ceiling well above where it had been. The practical effect is that the intergenerational transfer of the largest fortunes in the country will remain almost entirely untaxed for the foreseeable future, a decision made in the same law that phases in cuts to Medicaid and food assistance for the country's lowest earners.

A smaller, more sympathetic provision sits alongside it. Taxpayers 65 and older can claim an additional $6,000 standard deduction through 2028, a temporary benefit aimed at a specific, politically significant demographic. It is popular. It is also, like the SALT cap and the R&E fix, financed entirely through borrowing, since nothing elsewhere in the law offsets its cost.

Corporate AMT: a problem that got partially fixed

One thread of this story looked, for a while, like it might become a genuine embarrassment for the law's architects. The Corporate Alternative Minimum Tax (CAMT), a 15 percent minimum tax on large corporations' book income enacted separately in 2022, began interacting badly with the new Section 174A deductions. Because R&E costs are fully expensed for book purposes under standard accounting rules but had been amortized for tax purposes under the old TCJA regime, the transition created a mismatch: companies claiming large retroactive R&E deductions on their tax returns could simultaneously find themselves owing more under CAMT, because their book income wasn't dropping at the same rate as their taxable income.

Industry groups flagged the problem for months, and in some illustrative modeling, CAMT was projected to eat up as much as 32 percent of the tax savings a company might otherwise realize from its R&E deductions in a transition year. Critics on the other side argued that fixing it by regulation, rather than by statute, would amount to granting taxpayers a tax cut Congress never actually authorized.

Treasury and the IRS ultimately sided with the taxpayers. In February 2026, the agencies issued Notice 2026-7, which allows CAMT entities to reduce their adjusted financial statement income by domestic Section 174 amortization, largely neutralizing the double-counting problem for most affected corporations going forward. It is worth noting plainly: this was not a case of the tax code working as designed. It was a gap that industry lobbying closed through interim guidance, months after the law had already taken effect, and after companies had already been modeling around the uncertainty for the better part of a year.

The human cost: Medicaid and SNAP on a delayed fuse

The tax relief in OBBBA was front-loaded and, in places, retroactive. The spending cuts built into the same law to help offset that cost are running on an entirely different clock, and the gap between the two timelines is arguably the most consequential thing about the entire bill.

Medicaid work requirements do not take effect until January 1, 2027, and six-month eligibility redeterminations begin December 31, 2026. New out-of-pocket cost-sharing for expansion enrollees doesn't begin until October 2028. On the SNAP side, states begin absorbing a share of benefit costs for the first time starting in fiscal year 2028, with states carrying particularly high error rates permitted to delay even further, into 2029 or 2030.

Independent estimates of the scale involved vary, but they all point the same direction. CBO projects 11.8 million people will lose Medicaid coverage directly, with an additional 3.1 million losing adjacent marketplace coverage. The Urban Institute's modeling, focused specifically on the combined effect of work requirements and six-month redeterminations, projects enrollment declines of between 4.9 and 10.1 million people by 2028 depending on how aggressively individual states implement the new rules.

None of that has happened yet. It is scheduled. And that is precisely the point: the tax cuts already showed up in this year's refunds, while the offsetting cuts to the safety net are still more than a year away for most provisions, backloaded well past the point where most people connect one to the other.

The interest rate trap

Every dollar of revenue this law forgoes has to be borrowed, and borrowing at scale carries its own escalating price tag. Higher federal borrowing needs to place upward pressure on interest rates, which raises the cost of servicing not just the debt OBBBA creates but the roughly $31.5 trillion in existing federal debt already outstanding. CBO's own accounting captures this feedback loop directly: of the law's total projected cost, over $850 billion is interest expense alone, money that buys nothing except the privilege of having borrowed the rest.

That interest bill compounds. Debt held by the public is projected to reach 101 percent of GDP in 2026, on track to surpass the all-time World War II high of 106 percent of GDP by 2030, and to keep climbing well beyond that. This is not a one-time cost that resolves once the amended returns clear the IRS backlog. It is a structural feature of the law that will show up in federal budgets for years after most people have stopped thinking about OBBBA at all.

Where this leaves the ledger

Pull back far enough and two things are true at once, and a fair accounting has to hold both. The government's cash position this year is not collapsing. Revenue is up, the deficit is running below last year's pace, and the more alarming version of this story, the one built entirely around a single monthly deficit figure, does not hold up against the Treasury's own data.

But the underlying architecture of the law is exactly as costly as its critics warned, and arguably more so once the interest costs are fully priced in. A $4.7 trillion, ten-year hole doesn't announce itself in a single month's Treasury statement. It shows up gradually: in a corporate tax base that keeps eroding as amended returns clear the backlog, in an IRS too short-staffed to catch the fraud that inevitably rides along with a wave of retroactive refund claims, and in a set of safety-net cuts still more than a year from taking full effect.

The bill for OBBBA has not fully arrived. But the invoice, at $4.7 trillion and climbing, has already been written, and the country is going to be paying interest on it for a long time after the refund checks clear.

Share now

Key takeaways

- The Congressional Budget Office projects OBBBA will increase deficits by $4.7 trillion over the 2026-2035 budget window on a dynamic basis, including interest costs and macroeconomic effects.

- The law is projected to reduce federal revenue by $4.9 trillion and increase interest costs by over $850 billion through 2035.

- The federal deficit through the first eight months of FY2026 was $1.2 trillion, actually 9 percent lower than the same period in FY2025, driven by stronger individual income and payroll tax collections.

- Corporate income tax receipts fell 30 percent ($88 billion) in the same period, which Treasury attributes largely to OBBBA's business tax changes, including expanded R&E deductions.

- Small businesses with average gross receipts under $31 million could retroactively apply full R&E expensing to 2022, 2023, and 2024 returns, with amended filings due by July 6, 2026.

- The state and local tax (SALT) cap rose retroactively to $40,000 for 2025 and to roughly $40,400 for 2026, before reverting to $10,000 in 2030.

- The federal estate tax exemption rose to $15 million per person ($30 million per couple) starting January 1, 2026, permanently, with no scheduled sunset.

- The IRS workforce fell from about 102,000 to about 74,000 employees, a 27 percent reduction, during the same period the agency implemented over 100 tax code changes.

- The Budget Lab at Yale projects the 2025 IRS staffing cuts alone will reduce IRS revenues by nearly $600 billion over the 2026-2035 window due to lost enforcement capacity.

- A separate, unrelated Supreme Court ruling invalidated IEEPA tariffs in February 2026, triggering an estimated $166 billion in refunds to importers that also depressed May 2026 customs receipts.

- Treasury and the IRS issued Notice 2026-7 in February 2026, resolving most of the Corporate Alternative Minimum Tax conflict that had been offsetting R&E deduction benefits for large corporations.

- Major Medicaid and SNAP cuts remain scheduled, not yet in effect: Medicaid work requirements begin January 2027, and state SNAP cost-sharing does not begin until fiscal year 2028.

Sources

- Committee for a Responsible Federal Budget (CRFB) https://www.crfb.org/blogs/obbba-dynamic-score-comes-47-trillion

- Internal Revenue Service / National Taxpayer Advocate Annual Report https://www.irs.gov/newsroom/national-taxpayer-advocate-delivers-annual-report-to-congress-finds-taxpayer-service-was-strong-in-2025-but-foresees-challenges-for-taxpayers-who-encounter-problems-in-2026

- American Action Forum, Debt and Deficit Progress Report: May 2026 https://www.americanactionforum.org/insight/debt-and-deficit-lack-of-progress-report-may-2026/

- The Budget Lab at Yale, A Weakened IRS Has Substantial Consequences https://budgetlab.yale.edu/research/weakened-irs-has-substantial-consequences

- Congressional Budget Office, Monthly Budget Review: May 2026 https://www.cbo.gov/publication/61981

- Published 2026-07-13 03:00

- Modified 2026-07-13 03:00