-

Redaction

Redaction

Comparing the 50/30/20 rule and zero-based budgeting

An analytical breakdown of modern budgeting frameworks against the 2026 economic landscape of high interest rates, persistent inflation, and rising credit debt.

Effective personal finance management in 2026 demands more than passive observation - it requires active capital allocation. Two frameworks dominate the conversation: the 50/30/20 rule and zero-based budgeting (ZBB). Each uses different mechanics to pursue the same objective: solvency and long-term wealth accumulation. Choosing between them is not a matter of preference but a strategic decision shaped by your income volatility, debt load, and available time.

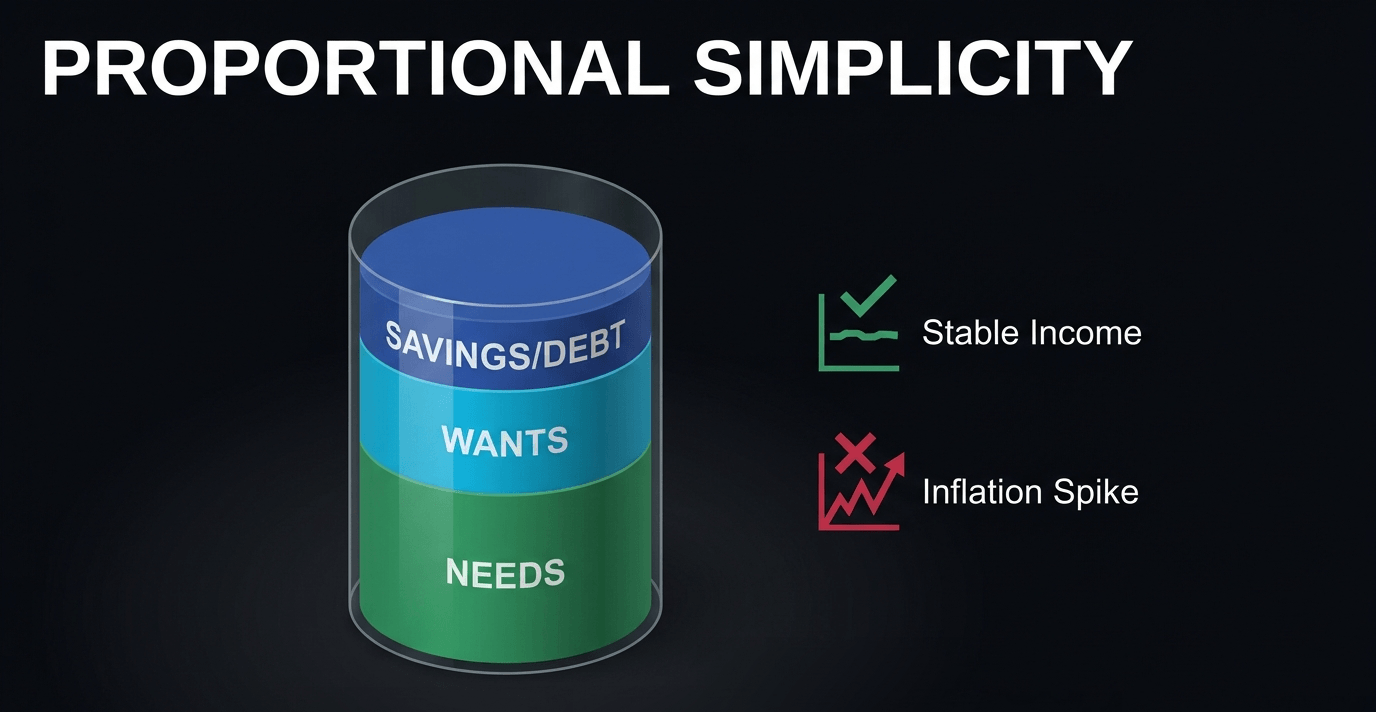

The 50/30/20 framework: proportional simplicity

The 50/30/20 rule, popularized by Senator Elizabeth Warren in her book All Your Worth, is a high-level heuristic for dividing after-tax income into three distinct buckets. Its core advantage is accessibility - no spreadsheets, no daily tracking, minimal friction.

How the three buckets work

Needs (50%) covers all non-discretionary expenses: housing, utilities, groceries, transportation, and minimum debt payments. In an environment where the Consumer Price Index rose 3.3% year-over-year as of March 2026, maintaining this ratio demands consistent discipline.

Wants (30%) addresses discretionary spending that improves quality of life - subscriptions, dining out, travel, and hobbies. This bucket is not frivolous; it serves as a psychological buffer against the burnout that accompanies extreme frugality, and it significantly improves long-term adherence to the system.

Savings and debt repayment (20%) is the engine of financial progress. Emergency fund contributions, retirement accounts (401(k), IRA), and accelerated debt principal payments all belong here.

Where the 50/30/20 rule works - and where it breaks down

This framework performs best for individuals with stable, predictable incomes and low-to-moderate debt loads. It operates as a practical "set and forget" system that flags structural imbalances immediately: if your needs bucket exceeds 50%, the math signals that something in your lifestyle architecture is misaligned.

However, the model assumes income stability that does not reflect the reality of many workers in 2026. For gig economy participants, freelancers, or anyone living in a high-cost-of-living urban center, the 50/30/20 split can feel like a framework designed for a different economic era. The gap between a $1,200 monthly rent in 2019 and a $2,100 rent in 2026 is not a rounding error - it is a structural problem the percentages alone cannot solve.

Zero-based budgeting: the precision of every dollar

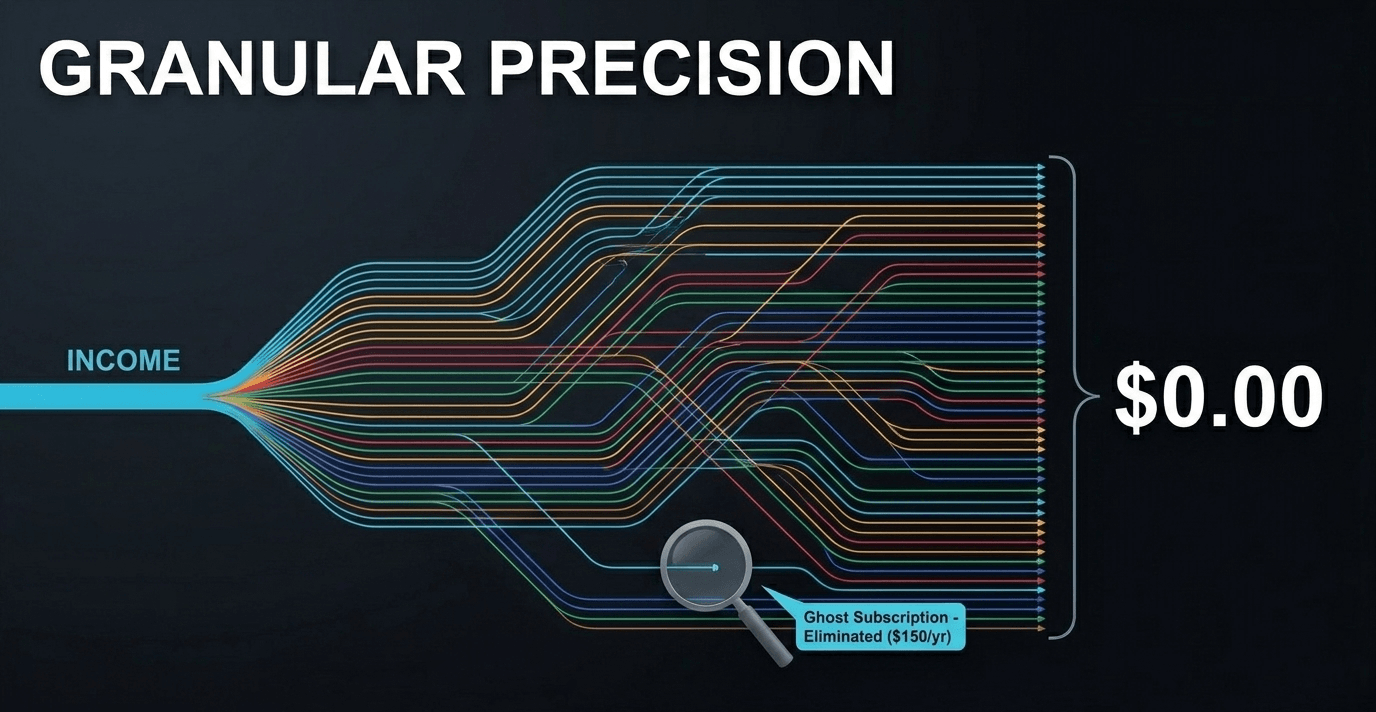

Zero-based budgeting (ZBB) operates on a fundamentally different premise: every dollar must be assigned a specific function before the month begins. The mathematical goal is straightforward - income minus expenses equals zero. Unlike traditional methods that carry forward prior spending habits with minor adjustments, ZBB demands fresh justification for every line item, every single period.

How zero-based budgeting works in practice

At the start of each budgeting period, you list your total income and then allocate every dollar across categories: fixed expenses, variable needs, discretionary wants, savings goals, and debt payments. Nothing is assumed. If you spent $80 on streaming services last month, that $80 must be re-justified this month.

This level of scrutiny is particularly effective during high-inflation periods. The 0.9% monthly surge observed in March 2026 makes it easy for costs to quietly compound. ZBB forces you to confront "ghost" subscriptions, redundant memberships, and spending drift that broader category budgets consistently miss.

The real trade-off with zero-based budgeting

The primary cost is time. Building a zero-based budget from scratch each month is resource-intensive - typically 1-3 hours depending on income complexity. For some, this administrative burden creates its own financial risk: the system gets abandoned within the first 60-90 days. Additionally, the month-by-month focus can lead users to deprioritize long-term investment contributions in favor of immediate cost-cutting, which can undermine retirement savings over time.

Economic context: the data shaping budgeting decisions in 2026

Budgeting decisions are never made in a vacuum. The macroeconomic environment of 2026 creates specific pressures that make the choice between these frameworks considerably more consequential than in previous years.

Interest rates and the true cost of debt

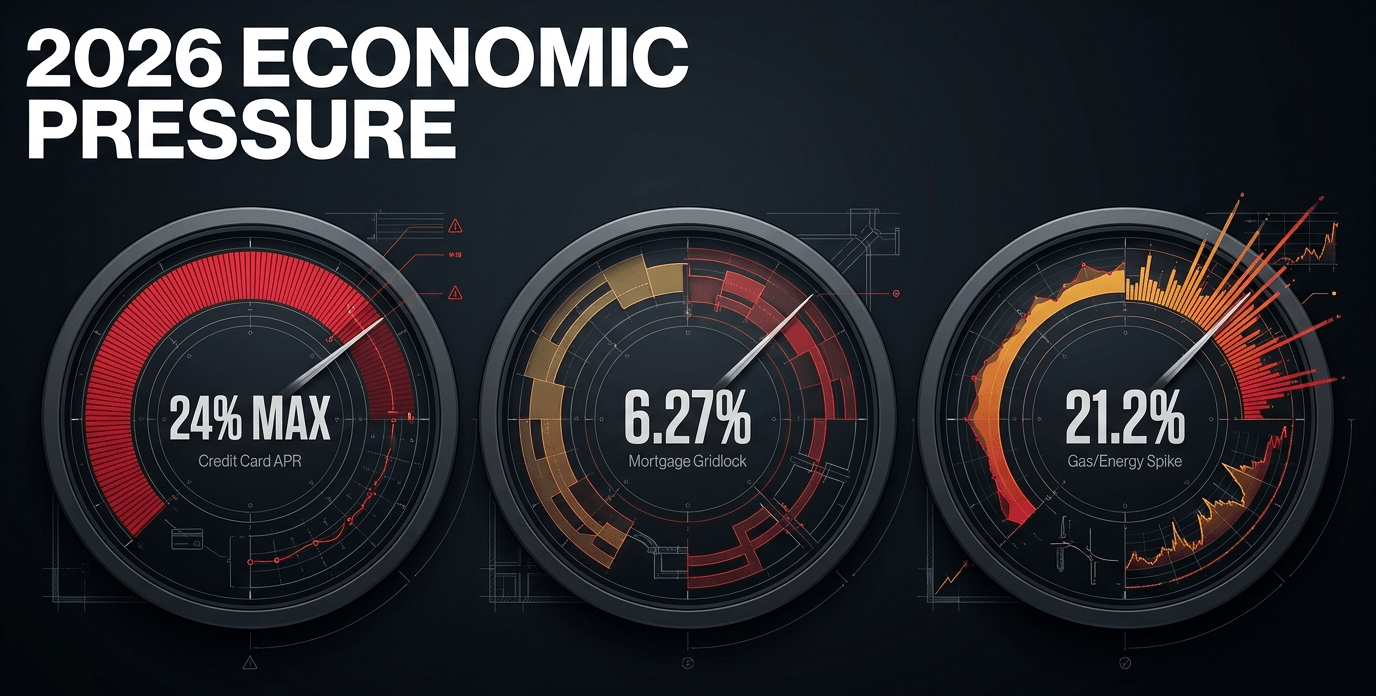

The Federal Reserve has maintained the federal funds rate at 3.50% to 3.75%. While a majority of policymakers anticipate a rate cut later in the year, today's reality for consumers is expensive borrowing. U.S. credit card debt has crossed the $1.33 trillion threshold, with average APRs hovering between 21% and 24% - historically elevated figures.

For 50/30/20 users, this places the 20% savings and debt bucket under enormous pressure. For ZBB practitioners, the mathematics are unambiguous: at 22% APR, a $5,000 balance costs approximately $1,100 per year in interest alone. Every unallocated dollar that does not go toward that balance is a guaranteed loss.

The housing and renovation pivot

A 30-year fixed mortgage rate of 6.27% has effectively frozen mobility for millions of homeowners. According to a Citizens Bank survey released April 23, 2026, only 13% of homeowners believe purchasing a new home is achievable in the current market. In response, 44% of homeowners are choosing to renovate their existing properties rather than relocate.

This behavioral shift carries direct budgeting implications. Renovations involve large, irregular capital outlays - precisely the type of spending that benefits from ZBB's granular, project-level tracking. A kitchen renovation that expands from $18,000 to $27,000 mid-project is far more manageable when every dollar has been pre-assigned and documented.

Inflationary volatility and 'needs' creep

Energy prices remain the primary driver of household budget volatility. A 21.2% monthly spike in gasoline prices has forced many households to reconsider the composition of their needs category. When fuel and utility costs surge, a rigid 50/30/20 split becomes structurally difficult to maintain - the needs bucket can swell to 60-70% of income, requiring a temporary contraction of wants or savings to compensate.

This is not a system failure. It is the system working as intended. The critical discipline is returning to target ratios as conditions normalize, rather than permanently accepting the inflated spending as the new baseline.

Strategic selection: matching the framework to your financial reality

Neither system is universally superior. Efficacy is entirely contingent on your operational reality - income pattern, debt load, behavioral tendencies, and available time.

When to use the 50/30/20 rule

The 50/30/20 rule is the right tool when you have a stable monthly income, a manageable debt-to-income ratio (ideally below 36%), and a primary goal of building long-term savings habits without daily administrative overhead. It is an excellent entry point for anyone who has never budgeted systematically before. Simplicity increases adherence, and sustained adherence outperforms perfect methodology applied inconsistently.

When to adopt zero-based budgeting

ZBB becomes the clearly superior choice in high-stakes financial scenarios. If you are a freelancer or contractor with variable monthly income, carrying high-interest debt with APRs above 20%, living paycheck to paycheck despite earning a reasonable salary, or managing a large one-time capital project like a home renovation - ZBB's granular accountability will surface spending leaks that proportional budgeting routinely masks. Even one eliminated "ghost" subscription recovered through ZBB scrutiny can save $150-$300 per year.

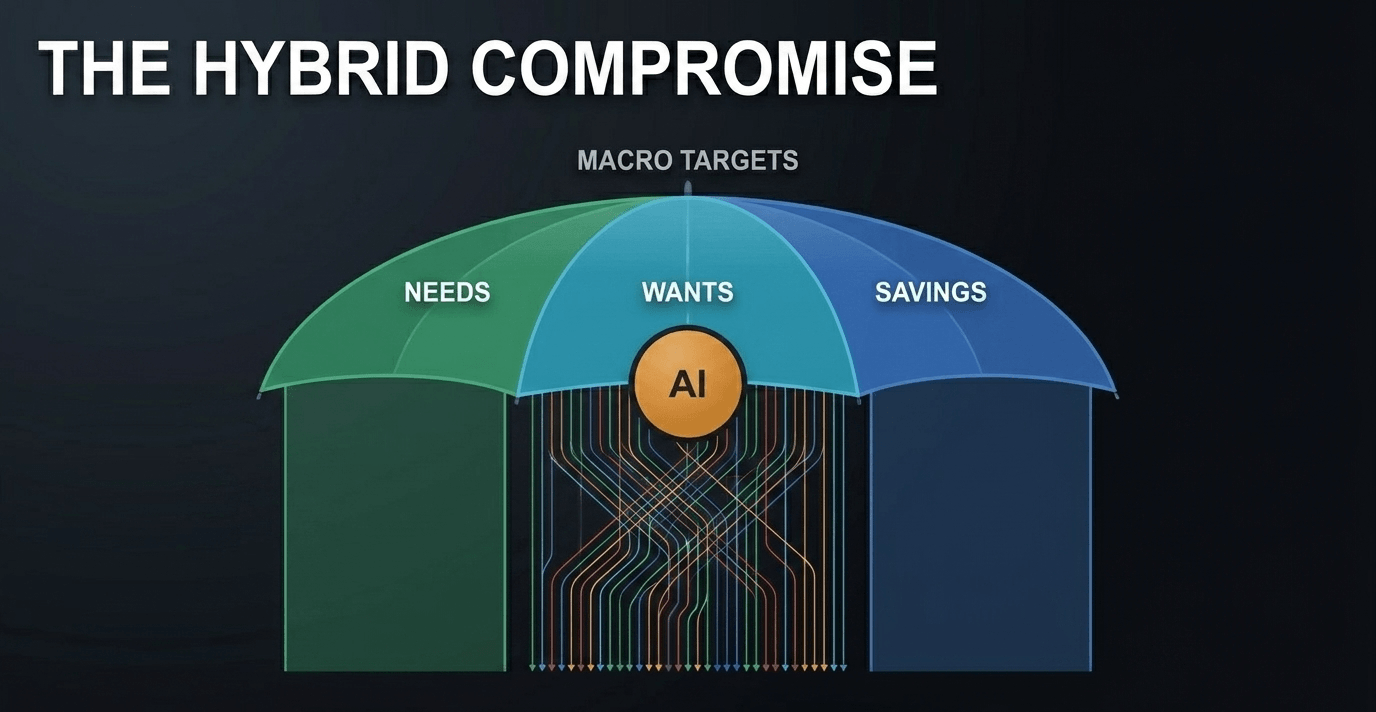

The hybrid approach: precision where it counts

A growing consensus among personal finance practitioners favors hybrid budgeting models. The strategy is straightforward: use the 50/30/20 rule to establish annual high-level targets, then apply ZBB principles exclusively to the wants category where lifestyle creep most commonly occurs.

This targeted precision delivers the best of both frameworks - minimal administrative friction for fixed costs, tight control over the discretionary spending that most frequently derails financial goals. AI-powered budgeting applications are making this hybrid approach increasingly practical by automating expense categorization and delivering real-time threshold alerts across both layers of the system.

Tools for implementing your budget in 2026

The framework you select matters less than your consistency in applying it. Several tools have made that consistency significantly easier:

For 50/30/20 practitioners, apps like Copilot and Monarch Money offer automatic income categorization by need, want, and savings - removing the manual sorting burden entirely. Both sync with bank accounts and alert you when any category approaches its limit.

For zero-based budgeting, YNAB (You Need a Budget) remains the benchmark tool. Its "give every dollar a job" philosophy is purpose-built for ZBB, and real-time multi-device sync makes the daily tracking requirement sustainable over the long term. EveryDollar by Ramsey Solutions is a strong, lower-cost alternative.

For hybrid approaches, tools that support multiple budget views - such as Monarch Money's customizable dashboard - allow proportional targets at the macro level alongside line-item control at the micro level.

Risk management in a volatile economy

Regardless of the budgeting method you adopt, the strategic priority in 2026 is risk mitigation through active capital deployment. With high-yield savings accounts (HYSAs) currently offering up to 4.21% APY, the opportunity cost of holding unallocated savings in a standard checking account is concrete and quantifiable.

Data from the Citizens Bank survey reflects a broader cultural shift: American consumers are becoming more pragmatic and defensive in their financial planning. The preference for renovation over relocation and the rising concern over utility costs indicate a meaningful transition from optimistic consumption to strategic capital preservation.

In this environment, your budget is no longer a static annual document. It is a dynamic operational tool that must adapt as inflation figures, interest rate forecasts, and personal income conditions evolve. Whether you choose the accessibility of the 50/30/20 rule, the rigor of zero-based budgeting, or an intelligent hybrid of both - the non-negotiable requirement is active, ongoing financial oversight.

Precision in capital allocation is not a luxury in 2026. It is the baseline strategy for protecting your purchasing power.

Frequently asked questions

What is the main difference between the 50/30/20 rule and zero-based budgeting? The 50/30/20 rule divides after-tax income into three percentage-based buckets - needs, wants, and savings - and works well for stable incomes and low-maintenance budgeting. Zero-based budgeting assigns every individual dollar a specific purpose each month, offering greater precision but requiring significantly more time and sustained discipline.

Which budgeting method is better for paying off debt quickly? Zero-based budgeting is generally the more effective tool for aggressive debt repayment. By scrutinizing every line item, ZBB identifies dollars that can be immediately redirected toward high-interest balances. With average credit card APRs between 21% and 24% in 2026, eliminating debt faster delivers a guaranteed return that no savings account can match.

Can I combine the 50/30/20 rule and zero-based budgeting? Yes - and many financial practitioners actively recommend it. The hybrid approach applies 50/30/20 targets for high-level annual goals, then uses ZBB-style tracking for the discretionary (wants) category where overspending most commonly occurs. AI-powered budgeting apps have made this combination increasingly easy to manage without significant time investment.

Does the 50/30/20 rule still work with high inflation in 2026? It remains a useful framework, but it requires contextual adjustment in high-cost environments. When energy prices spike or housing costs rise sharply, the needs bucket frequently exceeds 50%. In those periods, the rule should be treated as a target to return to, not a rigid constraint - temporarily reducing the wants allocation to 20% while the needs category normalizes.

What is the biggest risk of zero-based budgeting?

The primary risk is abandonment. The monthly time requirement - often 1-3 hours - causes many users to discontinue the practice within the first 60-90 days. A secondary risk is over-indexing on short-term cost elimination at the expense of long-term investment contributions, particularly retirement savings, which can compound into a significant financial shortfall over time.

Share now

Key takeaways

- The 50/30/20 rule allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment - making it one of the most accessible frameworks for personal budgeting.

- Zero-based budgeting (ZBB) requires every dollar to be assigned a specific purpose each month, with the goal of income minus all expenses equaling zero.

- U.S. credit card debt has reached $1.33 trillion, with average APRs between 21% and 24% - historically high levels that make active debt repayment a critical budget priority in 2026.

- The March 2026 Consumer Price Index rose 3.3% year-over-year, driven in part by a 21.2% monthly spike in gasoline prices, directly pressuring the needs category in percentage-based budgets.

- The Federal Reserve federal funds rate stands at 3.50%-3.75%, while 30-year fixed mortgage rates sit at approximately 6.27%, limiting housing market mobility.

- According to a Citizens Bank survey (April 2026), only 13% of homeowners believe buying a new home is currently achievable; 44% are choosing to renovate instead - a shift that favors the granular tracking of ZBB.

- High-yield savings accounts currently offer up to 4.21% APY, raising the measurable opportunity cost of holding unallocated savings in standard accounts.

- A hybrid budgeting approach - using 50/30/20 for high-level annual targets and ZBB for discretionary spending control - is an increasingly favored strategy among personal finance practitioners.

Sources

- Kudos https://www.joinkudos.com/blog/budgeting-methods-in-2025-50-30-20-vs-zero-based-vs-more---which-is-right-for-you

- Centier Bank https://www.centier.com/resources/articles/article-details/budget-smarts-in-2026--how-the-50-30-20-rule-works

- Easy Finance Insights https://easyfinanceinsights.wordpress.com/2025/10/14/50-30-20-rule-budgeting-guide/

- UNFCU Financial Wellness https://www.unfcu.org/financial-wellness/50-30-20-rule/

- Money Bites https://www.moneybites.com/post/pros-and-cons-of-the-50-30-20-budget-method

- Public.com https://public.com/learn/what-is-the-50-30-20-rule

- MMBB Financial Services https://www.mmbb.org/resources/e-newsletter/2024/july-august/zero-based-budgeting-and-the-50-30-20-rule

- WalletHub https://wallethub.com/edu/b/50-30-20-rule/144096

- Maps Credit Union https://www.mapscu.com/blogs/revisiting-50-30-20-for-2026/

- YouTube https://www.youtube.com/watch?v=-qxbzyz3iTg

- Paro AI https://paro.ai/blog/advantages-disadvantages-zero-based-budgeting/

- Financial Models Lab https://financialmodelslab.com/blogs/blog/what-difference-zero-based-budgeting-traditional-budgeting

- Prophix https://www.prophix.com/blog/zero-based-budgeting-pros-and-cons/

- Ringy https://www.ringy.com/articles/zero-based-budgeting

- Planacy https://planacy.com/en/blog/the-ultimate-guide-to-zero-based-budgeting-zbb-in-2024/

- The Wealth Break https://thewealthbreak.com/news/personal-finance-news-recap-april-2026s/

- Citizens Bank Investor Relations https://investor.citizensbank.com/about-us/newsroom/latest-news/2026/2026-04-23.aspx

- Published 2026-04-28 02:27

- Modified 2026-05-22 23:06

-

Redaction