-

Redaction

Redaction

How entrenched inflation psychology impacts prices

The University of Michigan reports record-low sentiment and rising inflation expectations as energy shocks from the Iran conflict alter consumer behavior.

The emergence of entrenched inflation psychology

Economic stability depends not only on current supply and demand - it hinges on what people collectively believe will happen next. As of April 2026, that collective psychology is actively driving real-world price increases, creating a dangerous feedback loop that policymakers are struggling to contain.

Data from the University of Michigan's Surveys of Consumers reveals a sharp deterioration in sentiment and a significant spike in inflation expectations. The critical shift underway is that the American public is no longer treating price increases as transitory fluctuations. They are being absorbed as a permanent fixture of economic life - and that belief, once entrenched, is extraordinarily difficult to reverse.

Why entrenched inflation expectations are so dangerous

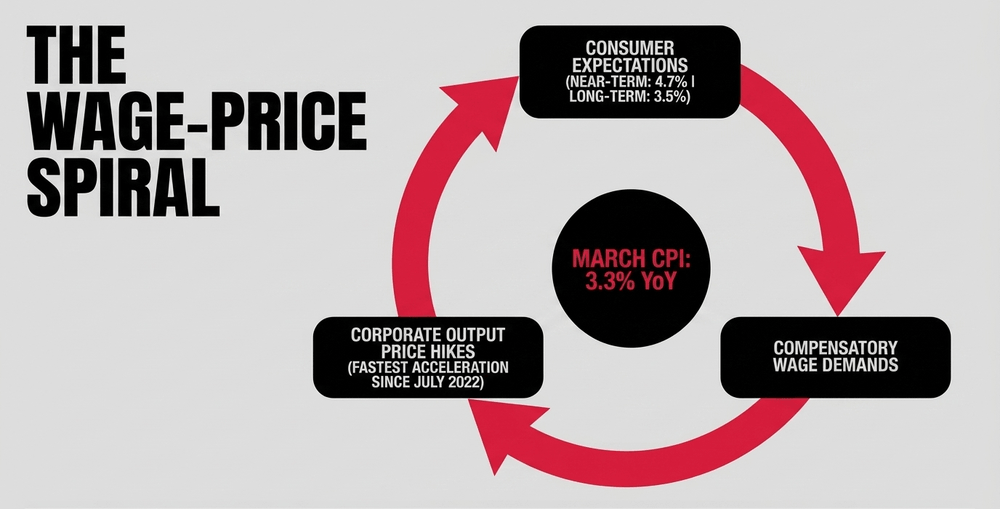

When consumers expect prices to rise, behavior changes immediately. Households accelerate purchases to beat future cost increases. Workers demand higher wages to protect their purchasing power. Businesses raise prices preemptively to protect margins. Each action independently fuels the very inflation being anticipated, creating a self-reinforcing wage-price spiral that monetary policy alone struggles to break.

This is precisely the dynamic the Federal Reserve fears most - and precisely what April 2026 data suggests is now forming.

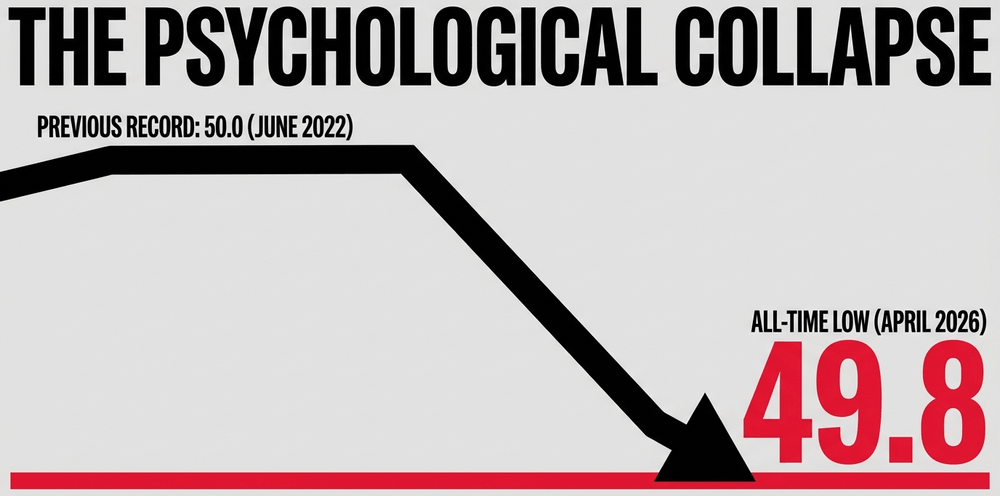

Consumer sentiment collapses to a record low

The University of Michigan Consumer Sentiment Index fell to a final reading of 49.8 in April 2026, marking an all-time low in the survey's history, which dates back to 1978. This represents a notable decline from 53.3 in March and surpasses the previous record low of 50.0 set in June 2022, during the peak of the post-pandemic inflation crisis.

Such a collapse in sentiment is not merely a statistical footnote. It signals a profound and broad-based erosion of economic confidence - driven primarily by the persistent destruction of household purchasing power and amplified by geopolitical shock.

Quantitative shifts in consumer expectations

The granular metrics within the April survey illustrate just how rapidly public perception is deteriorating.

Near-term inflation expectations - tracking what consumers anticipate for the next twelve months - surged to 4.7% in April from 3.8% in March. This single-month jump represents the largest one-month increase since April 2025 and far exceeds the 2.3% to 3.0% range that was considered normal during the two years before the COVID-19 pandemic.

Long-term five-year inflation expectations climbed to 3.5% in April, up from 3.2% in March - the highest reading since October 2025. This figure carries outsized significance for monetary policymakers. When workers price in 3.5% inflation over a five-year horizon, they demand compensatory wage increases. Employers then raise output prices to protect margins. The result is a structural ratchet that cannot be unwound without significant economic pain.

The Federal Reserve monitors these long-term figures with particular intensity precisely because they reveal whether inflation is becoming anchored in the public consciousness - the point of no return for a soft landing.

Geopolitical catalysts and energy market shocks

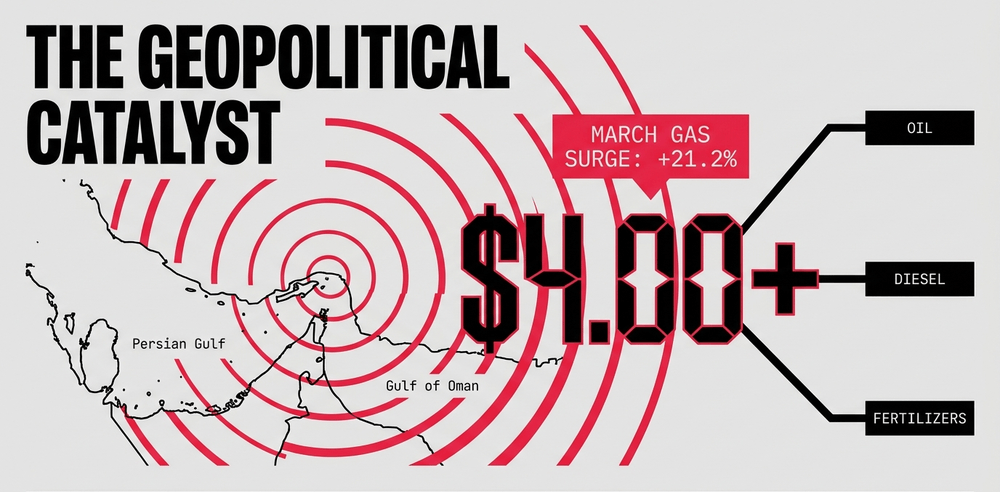

The primary accelerant behind this sentiment collapse is the ongoing conflict in Iran, which has caused significant disruption to shipping through the Strait of Hormuz - a chokepoint through which a substantial share of the world's seaborne oil transits daily.

The resulting supply constraints have pushed up prices across an interconnected chain of commodities: oil, gasoline, diesel, fertilizers, petrochemicals, and aluminum. National gasoline prices in the United States are currently hovering above $4 a gallon - a psychologically significant threshold that, historically, triggers immediate consumer distress and spending pullbacks.

Joanne Hsu, director of the Surveys of Consumers, noted that the Iran conflict influences consumer views primarily through shocks to gasoline and essential commodities. Gasoline occupies a unique psychological position in the inflation narrative: its price is displayed in large numerals on street corners, functioning as a daily, unavoidable reminder of inflationary pressure. Unlike price increases embedded in software subscriptions or service fees, energy costs hit household cash flow immediately and visibly - particularly for low- and middle-income families who allocate a disproportionately large share of disposable income to fuel and transport.

How high prices are eroding household living standards

The damage to personal finances is measurable and acute. According to the April University of Michigan survey, approximately half of all consumers spontaneously reported that high prices are actively eroding their standard of living - an unusually high proportion for this measure. Personal finance assessments dropped by roughly 11% in April alone.

This reflects the core distinction between nominal and real income. Wages may be growing in headline terms, but when price increases outpace those gains, households are effectively earning less in terms of what their money can actually buy. The result is a quiet, grinding reduction in living standards that does not show up in employment statistics but is felt acutely at the household level.

Data from S&P Global reinforces this picture. A key measure of prices charged by businesses for goods and services jumped in April to the highest level since July 2022 - the fastest rate of price acceleration in nearly four years. These input costs are being passed directly to consumers rather than absorbed into corporate margins.

The overall Consumer Price Index (CPI) rose to 3.3% year-on-year in March 2026, up sharply from 2.4% in February. Gasoline prices, which surged 21.2% in March alone, accounted for nearly three-quarters of that monthly CPI increase. This concentration of inflationary pressure in energy creates a regressive burden: essential mobility becomes dramatically more expensive, and those least able to absorb the cost bear the largest share of it.

The Federal Reserve's constrained policy options

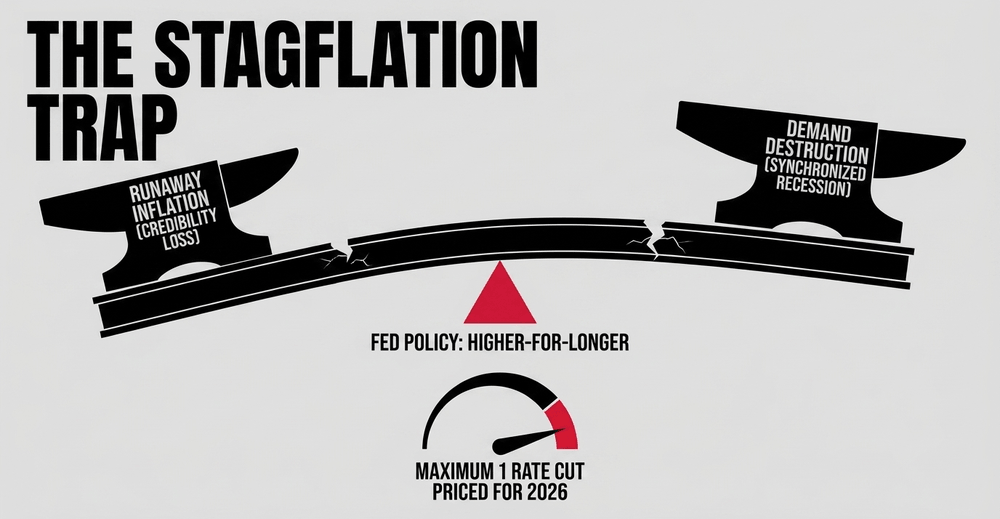

Rising inflation expectations have materially altered the outlook for Federal Reserve rate policy in 2026. Earlier in the year, financial markets were pricing in a meaningful series of interest rate cuts as inflation appeared to be normalizing toward the Fed's 2% target. That scenario has now been effectively shelved.

The current consensus is that the Federal Reserve will make at most one modest rate adjustment throughout 2026. The central bank's own March 2026 Summary of Economic Projections placed core PCE inflation at 2.7% for the year - but deteriorating consumer conditions and rising energy costs suggest meaningful upside risk to that forecast.

The Fed's core challenge is a classic policy dilemma. To combat entrenched inflation expectations, it may need to signal an aggressively hawkish stance - research consistently shows that credible commitment to price stability can lower market-based inflation expectations, particularly at longer horizons. However, maintaining elevated interest rates for a sustained period carries its own risks: a potential over-tightening that chokes consumption growth, slows hiring, and tips the economy toward recession.

Economists note that the demand destruction from elevated gasoline prices may already be functioning as a natural brake on spending - reducing the immediate urgency for additional rate hikes while simultaneously increasing the risk of stagflation if growth deteriorates faster than inflation does.

Stagflation risk: what the data is signaling

The word stagflation - the toxic combination of stagnant growth and persistent inflation - has re-entered serious economic discussion for the first time since the 1970s. The current configuration of indicators is not yet stagflationary, but several warning signs are flashing simultaneously:

- Consumer sentiment is at a historic low, signaling suppressed demand ahead

- Inflation expectations are rising at the fastest pace in over a year

- Energy price shocks are functioning as a tax on consumption, reducing real spending capacity

- Businesses are raising output prices at the fastest rate since mid-2022, suggesting cost pressures are structural, not temporary

- The Federal Reserve has limited room to cut rates without risking a credibility loss on inflation

Whether this environment tips into genuine stagflation will depend heavily on the trajectory of the Iran conflict and the speed of any energy market normalization.

Global supply chain and industrial cost implications

The inflationary pressure extends well beyond the consumer retail sector. Elevated diesel prices increase the cost of moving freight across logistics networks, raising the baseline cost of delivering nearly every physical good. High fertilizer prices - which are derived from natural gas - are being baked into the next agricultural production cycle, strongly suggesting that food price pressures will materialize in the second half of 2026 regardless of how quickly energy markets stabilize.

Meanwhile, increases in petrochemical and aluminum prices are working their way through manufacturing supply chains in automotive, packaging, and consumer electronics. Firms facing higher input costs must choose between margin compression and price increases. S&P Global data indicates most are choosing the latter - passing costs downstream to end consumers rather than absorbing them.

Central banks globally are responding by maintaining current borrowing rates in a wait-and-see posture, attempting to avoid the wage-price spirals that defined the inflationary decade of the 1970s. The risk of acting too slowly is that expectations become self-fulfilling; the risk of acting too aggressively is that a coordinated global tightening cycle triggers a synchronized recession.

What consumers and investors should consider now

For households, the most actionable near-term response to an entrenched high-inflation environment involves reassessing fixed versus variable rate debt exposure, prioritizing spending on non-discretionary essentials, and stress-testing budgets against scenarios where gasoline remains above $4 per gallon through the remainder of the year.

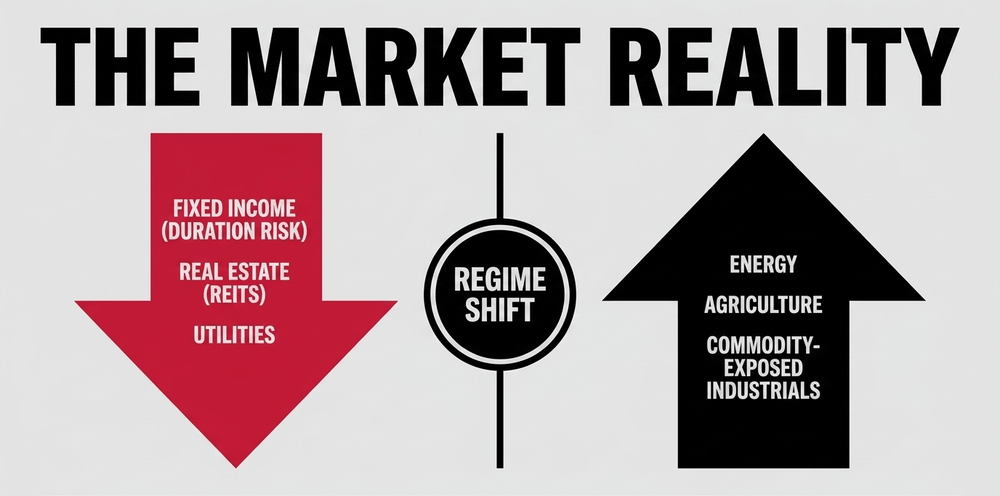

For investors, a sustained higher-for-longer interest rate environment has direct implications for asset allocation. Duration risk in fixed income portfolios increases as rate cut expectations are priced out. Equities in sectors with pricing power - energy, agriculture, and industrials with commodity exposure - tend to outperform in inflationary cycles, while rate-sensitive sectors such as real estate investment trusts and utilities face headwinds.

The critical variable to monitor is whether long-term inflation expectations remain below 4%. A sustained breach of that level would represent a significant loss of Fed credibility and would likely trigger a material policy response - with consequences for borrowing costs across mortgages, auto loans, and business credit.

The path forward: credibility is everything

Success in containing this inflationary episode will ultimately hinge on one factor: whether the Federal Reserve can credibly convince the public that price stability is achievable and actively being defended.

If near-term consumer expectations continue climbing toward the 5% mark, the pressure on the Fed to maintain rates at restrictive levels will become politically and economically insurmountable. The Consumer Sentiment Index at a historic low of 49.8 represents a fragile psychological foundation - one that could deteriorate further if energy prices remain elevated or if the Middle East conflict intensifies.

Without a meaningful de-escalation of the Iran conflict or a stabilization of global energy markets, the risk of a prolonged stagflationary environment increases materially. Businesses and investors navigating this environment should plan for sustained high borrowing costs, continued energy price volatility, and a Federal Reserve that prioritizes the anchoring of inflation expectations above all other policy objectives - including the stimulation of growth.

Share now

Key takeaways

- The University of Michigan Consumer Sentiment Index collapsed to a record low of 49.8 in April 2026 - the weakest reading in the survey's history, which dates back to 1978, falling below the previous all-time low of 50.0 set in June 2022.

- Near-term 12-month inflation expectations surged to 4.7% in April from 3.8% in March - the largest single-month increase since April 2025, far exceeding the 2.3%-3.0% pre-pandemic baseline.

- Long-term 5-year inflation expectations rose to 3.5% in April, up from 3.2% in March - the highest reading since October 2025 and a key trigger for potential wage-price spiral dynamics.

- Disruptions to shipping through the Strait of Hormuz, caused by the conflict in Iran, pushed national U.S. gasoline prices above $4 per gallon for the first time since 2022.

- Gasoline prices surged 21.2% in March 2026 alone, accounting for nearly three-quarters of that month's total CPI increase.

- Approximately half of all surveyed consumers spontaneously reported that high prices are actively eroding their standard of living, with personal finance assessments dropping ~11% in April alone.

- S&P Global data shows business output price gauges reached their highest level since July 2022 in April 2026 - the fastest rate of price acceleration in nearly four years.

- Overall CPI inflation rose to 3.3% year-on-year in March 2026, a significant acceleration from 2.4% in February.

- The Federal Reserve's March 2026 Summary of Economic Projections places core PCE inflation at 2.7% for the year - though deteriorating consumer conditions point to meaningful upside risk to that estimate.

- Financial markets now anticipate the Federal Reserve will make at most one modest rate adjustment in 2026, a sharp pullback from earlier expectations of multiple cuts.

Sources

- University of Michigan Surveys of Consumers https://www.sca.isr.umich.edu/

- Bureau of Labor Statistics - CPI March 2026 https://www.bls.gov/news.release/cpi.nr0.htm

- Federal Reserve - March 2026 Summary of Economic Projections https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20260318.htm

- CNBC - Consumer sentiment, inflation fears and the Iran conflict (April 2026) https://www.cnbc.com/2026/04/10/consumer-sentiment-inflation-fears-iran-war.html

- CNBC - CPI inflation report March 2026 https://www.cnbc.com/2026/04/10/cpi-inflation-report-march-2026.html

- Advisor Perspectives (dshort) - Michigan Consumer Sentiment plunges to record low, April 2026 https://www.advisorperspectives.com/dshort/updates/2026/04/10/consumer-sentiment-plunges-to-lowest-level-on-record

- S&P Global - US Composite PMI April 2026 https://www.pmi.spglobal.com/Public/Home/PressRelease/8bdf1bb2dddf420e9c0e9d7e22f75c09

- Published 2026-04-28 22:02

- Modified 2026-05-23 02:16

-

Redaction